Updated December 5, 2005

December 5, 2005

Military personnel on

active duty are being overcharged on high interest loans by some of the

largest banks in the United States, a new investigation of compliance

with the Servicemembers’ Civil Relief Act (SCRA) by Inner City Press /

Fair Finance Watch has uncovered. Through documents obtained under the

Freedom of Information Act, ICP had documented widespread violations of

the SCRA, defrauding and overcharging of those in active military

service, and regulatory inertia in dealing with the abuses.

The nation’s largest

bank, Citigroup,

is described in consumers’ complaints as demanding original copies of

initial deployment orders, of refusing to deal by telephone with

servicemembers’ immediate relatives, and of reporting adversely to

credit agencies. HSBC

/ Household is described as seeking to narrow SCRA’s interest rate

reductions to only those “in a hostile zone,” leaving that term

undefined. Other banks most complained-of include

JP Morgan Chase,

Wells Fargo, MBNA

and Bank of America.

Regarding these last two, ICP has asked the

Federal Reserve

to collect and consider the evidence of SCRA violations before ruling on

the Bank of America – MBNA merger application.

The Servicemembers’ Civil Relief Act,

at 50 USCS Appendix Section 527(1)(a)

provides that “An obligation or liability bearing interest at a rate in

excess of 6 percent per year that is incurred by a servicemember, or the

servicemember and the servicemember's spouse jointly, before the

servicemember enters military service shall not bear interest at a rate

in excess of 6 percent per year during the period of military service.”

The purpose of the SCRA, formerly known as the Soldiers’ and Sailors’

Civil Relief Act, is to provide interest rate relief and other

protections “to servicemembers of the

United States to enable such persons to devote their entire energy to

the defense needs of the Nation.” Section 502.

The above-named banks, however,

routinely seek to deny the SCRA protections to servicemembers.

Citigroup, for example, beyond deployment orders has demanded original

enlistment papers, as reflected in this complaint to

Citigroup’s AT&T

Universal credit card unit in Jacksonville, Florida, now placed online

at

www.innercitypress.org/citiscra4.jpg

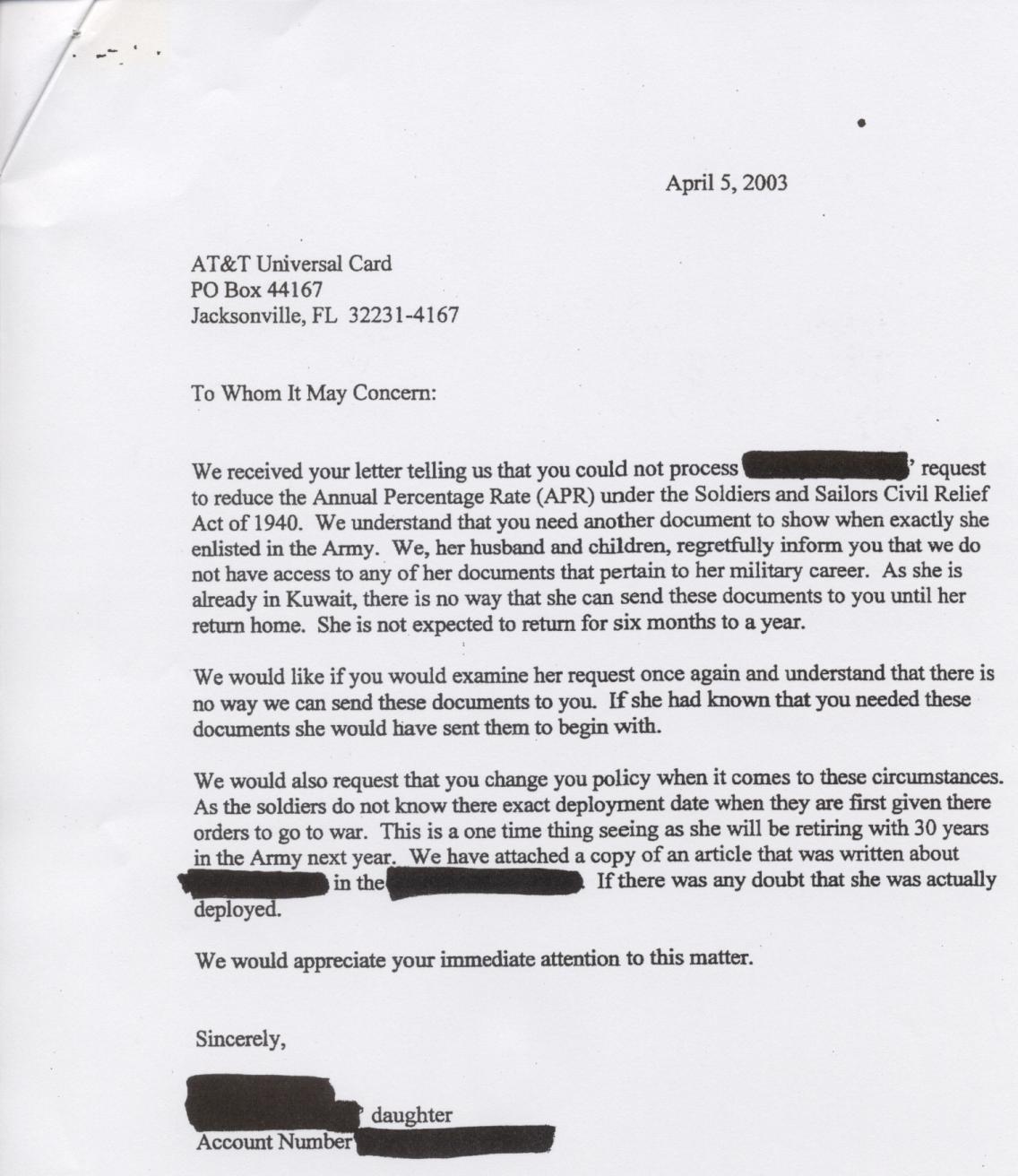

“We received your letter

telling us that you could not process [REDACTED]’s request to reduce the

Annual Percentage Rate (APR) under the Soldiers and Sailors Civil Relief

Act of 1940. We understand that you need another document to show when

exactly she enlisted in the Army. We, her husband and children,

regretfully inform you that we do not have access to any of her

documents that pertain to her military career. As she is already in

Kuwait, there is no way that she can send these documents to you until

her return home. She is not expected to return for six months to a

year.”

Using prior military service as an

excuse to maintain high interest rates despite the SCRA appears to the

strategy as other Citibank units as well, as reflected by the complaint

to Citibank’s regulator, the Office of the Comptroller of the Currency (OCC),

now online at

www.innercitypress.org/citiscra4.jpg

“I am writing in

regards to a dispute with The Associates credit card company of Citicorp

Credit Services, Inc. (USA). The dispute pertains to my eligibility to

receive the interest credit from the Sailors’ and Soldiers’ Relief Act (SSCRA)

(50 U.S. App. Sec. 526).

“I first contacted The

Associates in May of 2002. At that time I was denied enrollment. I was

told that because I originally entered the military in 1989, I was

ineligible. However, my tour of duty was over in 1993. I opened my

account with The Associates in 2000. At that time, I was a civilian and

had no intentions of signing back up with the military. Yet, in March of

2002, I entered into the US Army on full-time, active military duty. As

the law states, the SSCRA regulates the amount of interest I am to be

charged for any credit accounts I opened before entry into military

service.

"I have disputed this

matter with The Associates to no avail. I have sent them copies of my

original orders showing my current enlistment date, as well as a copy of

the law. Still I was denied. I was then forced to go to my JAG office on

base to seek legal counsel. From there I was directed to the Attorney

General’s office in Irving, TX, the headquarters for the aforementioned

party. The Attorney General’s office then put me in touch with the legal

representatives of the [REDACTED] County, where I received contact

information for the OCC Customer Assistance Group.

"The Associates have

repeatedly denied my claims based on prior service. Yet, I have found

nowhere in the law where it states this as a deciding factor. So I write

to you now, to examine the law and enforce the necessary actions. I have

enclosed all pertinent documents in regard to this matter. I have been

enrolled in a debt consolidation company, and have made payments to The

Associates monthly for the last year.”

The attachment, on

Department of the Army stationary, reflects Citigroup’s Associates

charging 12.99% interest. In April 2005, a mother wrote to the OCC, in

a letter now online now online at

www.innercitypress.org/citiscra12.jpg

“Enclosed is a copy of my son’s military orders

calling him to active duty, a copy of the affidavit designating me as

his authorized representative, and a copy of my letter to Citibank,

Sioux Falls, SD, dated 8 December, 2004. Citibank has given me all kinds

of excuses for not acting on this matter. First they wanted an affidavit

specifically addressed to them. They desisted on their request once I

explained to them that the military do not have the time and manpower to

prepare affidavits in the manner Citibank wanted. Then they told me that

my son’s active duty orders were not with the correspondence I had

mailed them. Then they said I needed to prepare a document which they

were going to mail to me; I have never received such document. Last time

I called I was told that they were still investigating!”

Another mother

complained:

…”His unit was deployed

to the Middle East. In February 2003 his fiancé and I applied to

Citibank to have his finance charges reduced under the Soldier’s and

Sailor’s Relief Act of 1940. (Account # [REDACTED]). We have supplied

Citibank with several letters of proof of my son’s service (copy of one

enclosed) with no satisfaction. We recently received a letter requesting

a “Proof of Service Letter” from Citibank. While the people at Citibank

that I have spoken with are polite and helpful, nothing has been

accomplished. Telephone calls to the customer service number are no help

as the group that handles Soldier’s and Sailor’s Act requests are in

Jacksonville, FL and can’t be reached by telephone, only by mail. I

think the enclosed letter (which Citibank already has) from the

Headquarters of II MEF should be sufficient proof of my son’s service

and that Citibank’s foot dragging is nothing more than an attempt on

their part to make the process so long and drawn out so that we will

give up as they do not want to lose the 24.24% interest that is being

paid on the account.”

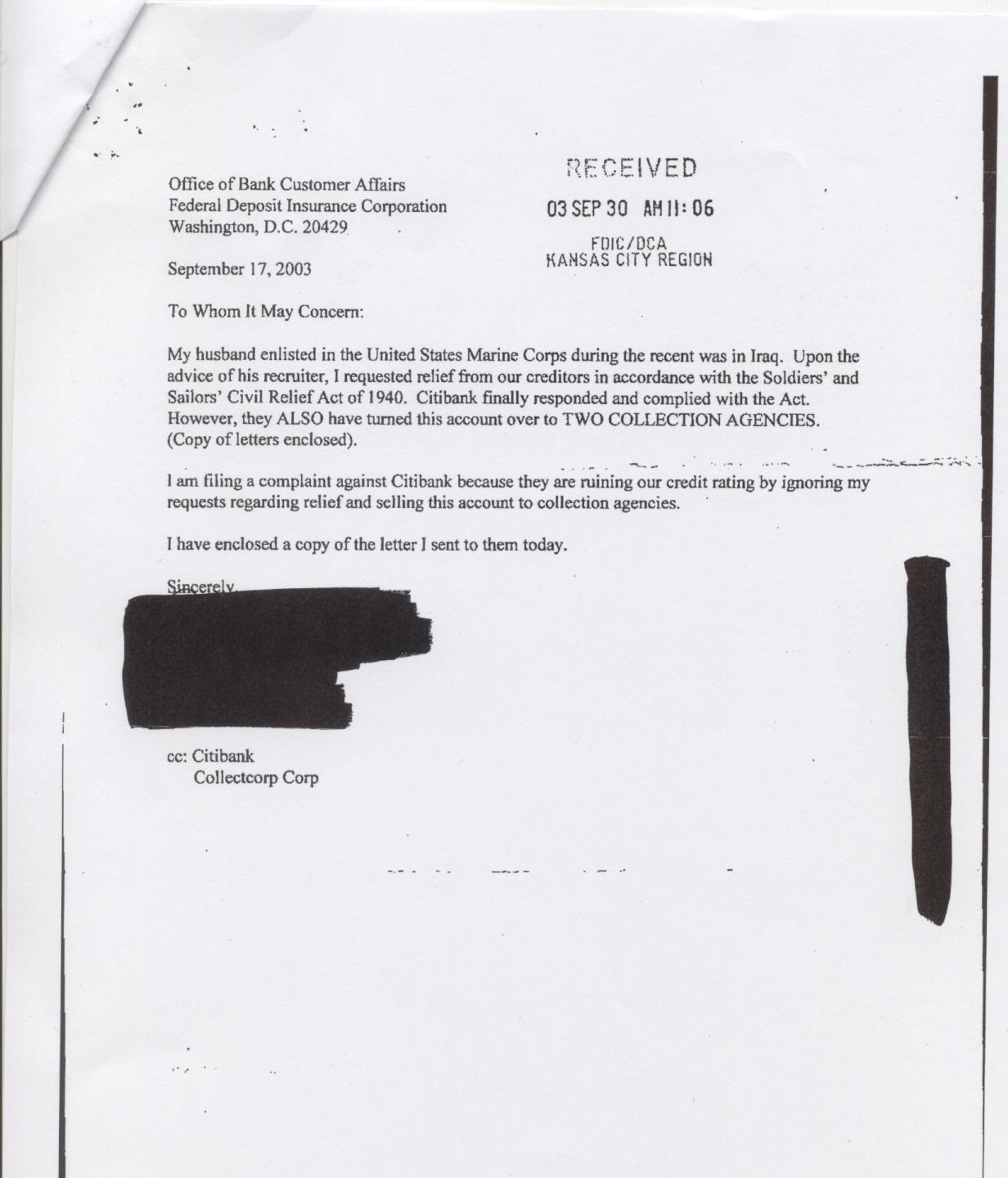

Even when compliance is belatedly obtained from

Citigroup,

accounts are still turned over to collection agencies, and credit

ratings impacted, as reflected in this complaint to the FDIC, placed

online at

www.innercitypress.org/citiscra5.jpg

“My husband enlisted in

the United States Marine Corps during the recent war in Iraq. Upon the

advice of his recruiter, I requested relief from our creditors in

accordance with the Soldiers’ and Sailors’ Civil Relief Act of 1940.

Citibank finally responded and complied with the Act. However, they ALSO

have turned this account over to TWO COLLECTION AGENCIES (copy of letter

enclosed).

“I am filing a complaint

against Citibank because they are ruining our credit rating by ignoring

my requests regarding relief and selling this account to collection

agencies.”

The attached notice – even the name of the

collection agency has been redacted by the Office of the Comptroller of

the Currency – reflects a balance of $1,937.13. It begins: “This is to

advise you that Citibank (South Dakota) Na (P) has transferred your

delinquent account to our office for pre-legal collection.”

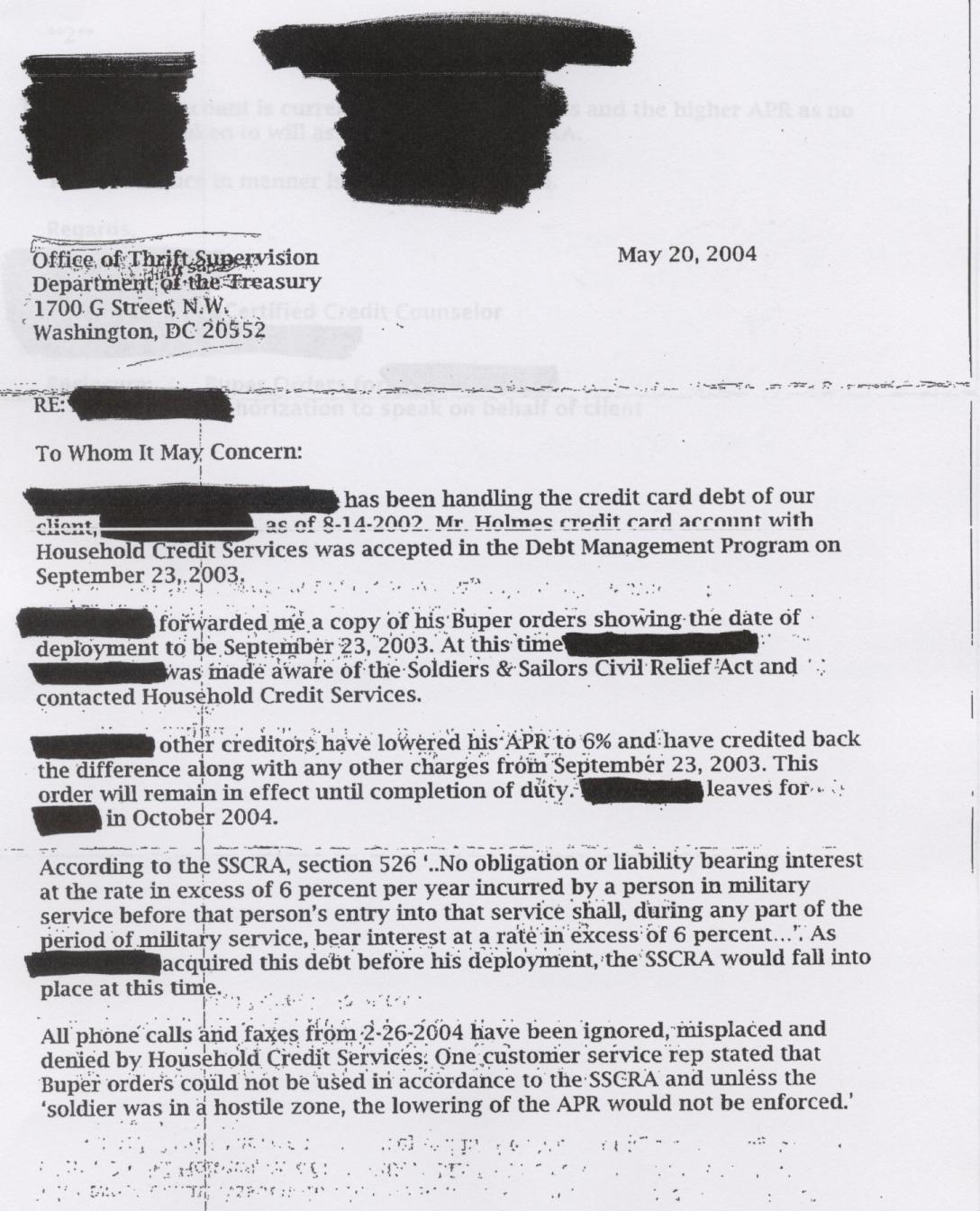

HSBC’s subprime

consumer finance units, operating under names including Household, HFC,

Beneficial and Orchard Bank, also stretch to find excuses to maintain

high interest rates contrary to the SCRA, as reflected by this sample

complaint now online at

www.innercitypress.org/hsbcscra15a.jpg and

www.innercitypress.org/hsbcscra15b.jpg

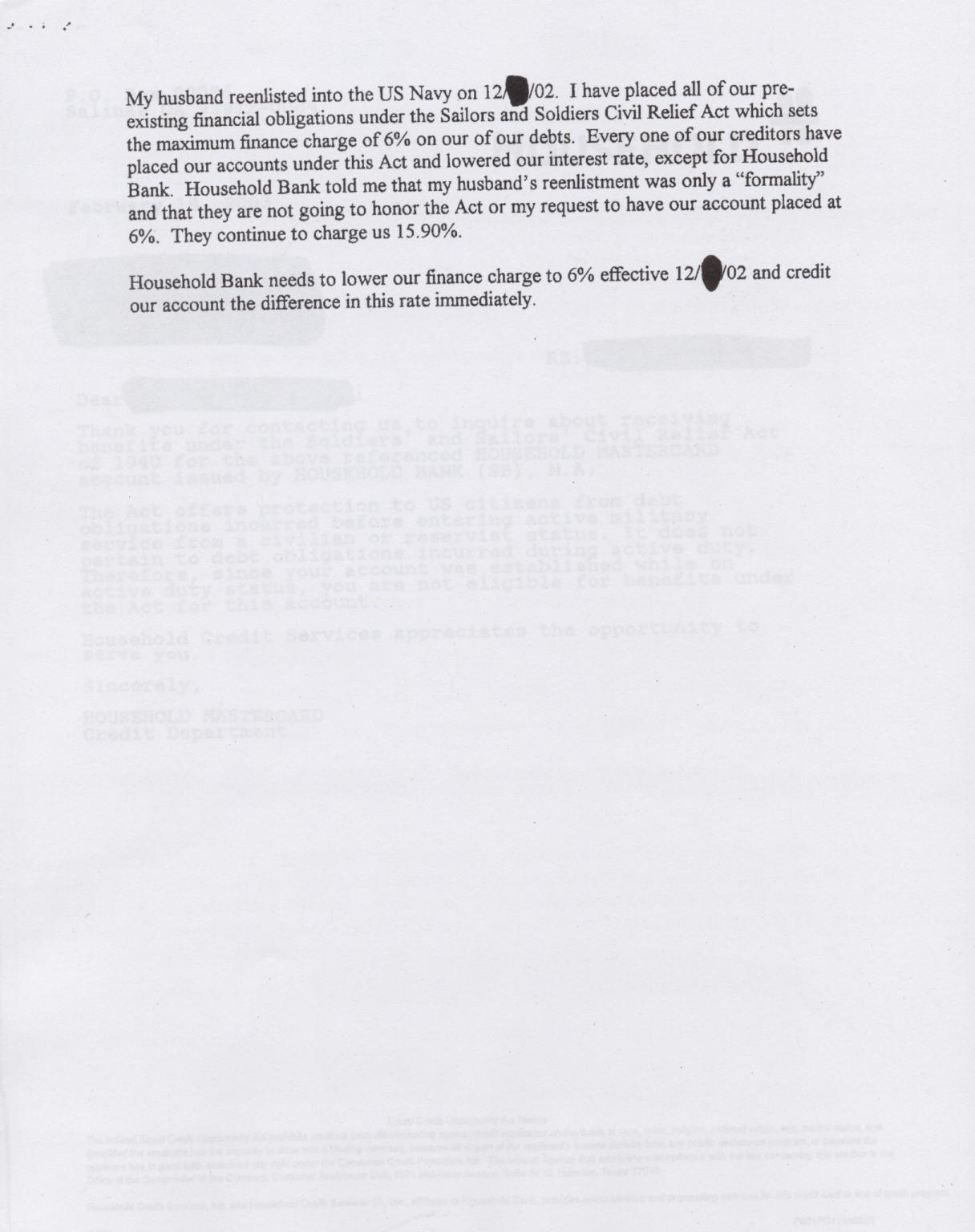

“My husband reenlisted

into the US Navy on 12/[ ]/02. I have placed all of our pre-existing

financial obligations under the Sailors and Soldiers Civil Relief Act

which sets the maximum finance charge of 6% on all of our debts. Every

one of our creditors have placed our accounts under this Act and lowered

our interest rate, except for Household Bank. Household Bank told me

that my husband’s reenlistment was only a ‘formality’ and that they are

not going to honor the Act or my request to have our account placed at

6%. They continue to charge us 15.90%.”

Contrary to the above-quoted language of the SCRA

(applying to “the period of military

service”),

HSBC’s Household came up with the novel argument, reflected in the

complaint now online at

www.innercitypress.org/hsbcscra18.jpg that the interest

rate must only be reduced if the soldier is in a “hostile zone” –

“All phone calls and

faxes from 2-26-2004 have been ignored, misplaced and denied by

Household Credit Services. One customer service rep stated that Buper

orders could not be used in accordance to the SSCRA and unless the

‘soldier was in a hostile zone, the lowering of the APR would not be

enforced.’”

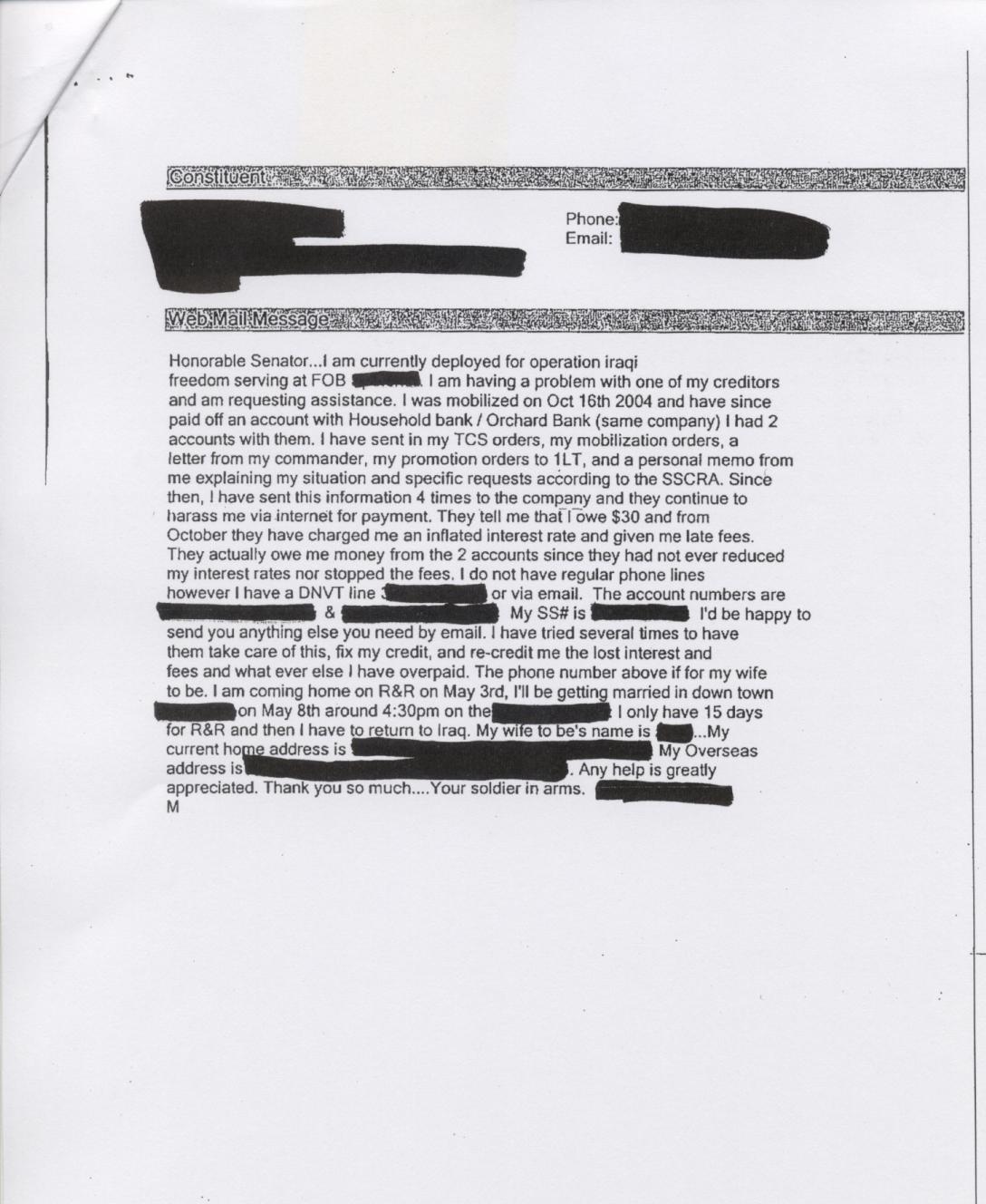

Even to those in “hostile zones,” HSBC sends

bill collection notices over the Internet, as reflected in the May 2005

complaint now online at

www.innercitypress.org/hsbcscra22.jpg

“I am currently deployed

for operation Iraqi freedom serving FOB [REDACTED]. I am having a

problem with one of my creditors and am requesting assistance. I was

mobilized on October 16, 2004 and have since paid off an account with

Household Bank / Orchard Bank (same company) I had 2 accounts with them.

I have sent in my TCS orders, my mobilization orders, a letter from my

commander, my promotion orders to 1LT, and a personal memo from my

explaining my situation and specific requests according to the SSCRA.

Since then, I have sent this information 4 times to the company and they

continue to harass me via internet for payment. They tell me that I owe

$30 and form October they have charged me an inflated interest rate and

given me late fees. They actually owe me money from the 2 accounts since

they had not ever reduced my interest rates nor stopped the fees. I do

not have regular phone lines however I have a DNVT line [REDACTED] or

via email…. Your soldier in arms.”

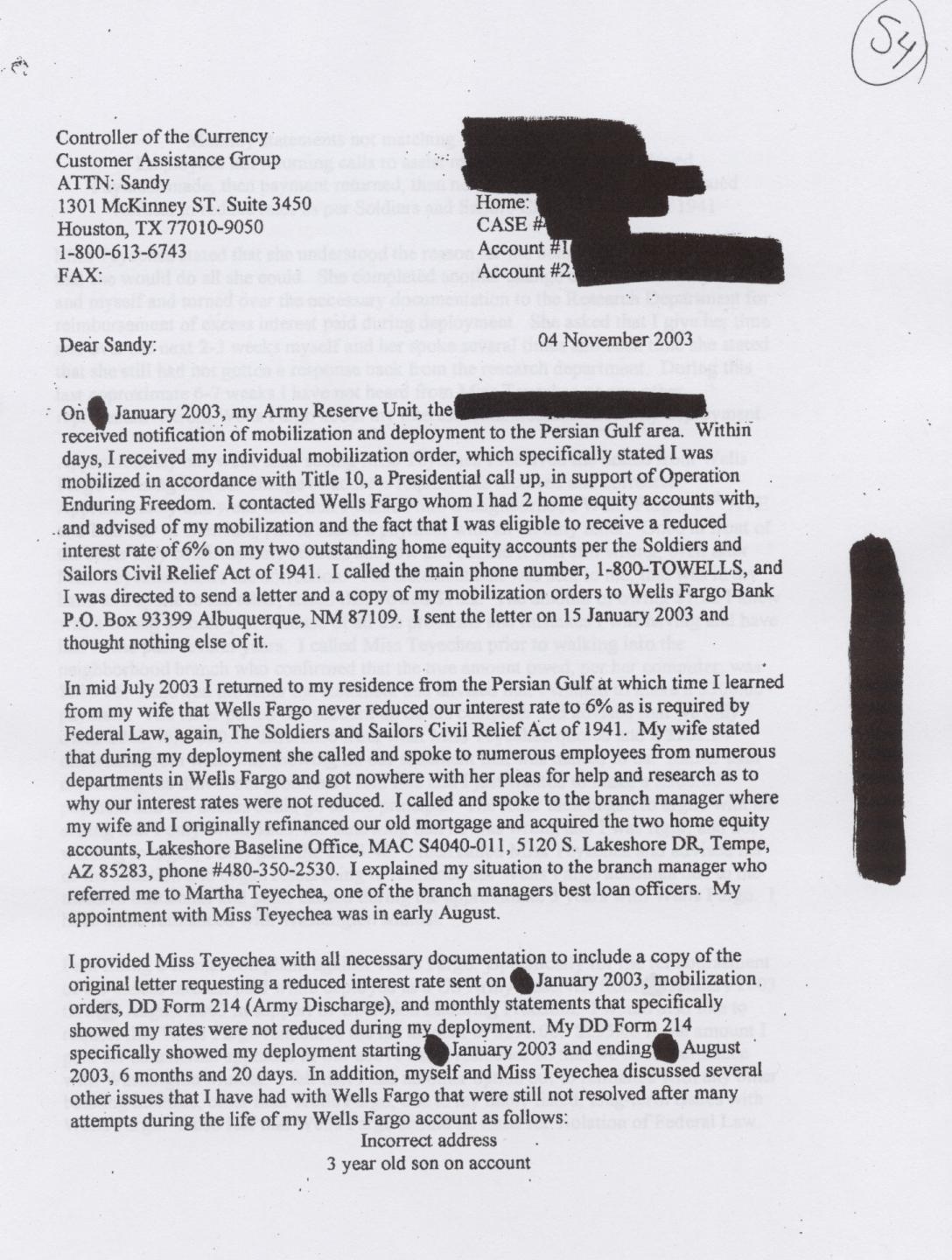

Wells Fargo’s

practices are reflected in the complaint to the OCC now online at

www.innercitypress.org/wellsscra54.jpg

“On [ ] January 2003, my

Army Reserve Unit, the [REDACTED] received notification of mobilization

and deployment to the Persian Gulf area. Within days I received my

individual mobilization order, which specifically stated I was mobilized

in accordance with Title 10, a Presidential call up, in support of

Operation Enduring Freedom. I contacted Wells Fargo whom I had 2 home

equity accounts with, and advised of my mobilization and the fact that I

was eligible to receive a reduced interest rate of 6% on my two

outstanding home equity accounts per the Soldiers and Sailors Civil

Relief Act of 194[0]… In mid July 2003 I returned to my residence from

the Persian Gulf at which time I learned from my wife that Wells Fargo

never reduced our interest rate to 6% as is required by Federal law…”

Wells Fargo is also,

like JP Morgan Chase and Bank of America, a funder of payday lenders,

including targeters of military personnel like Armed Forces Loans.

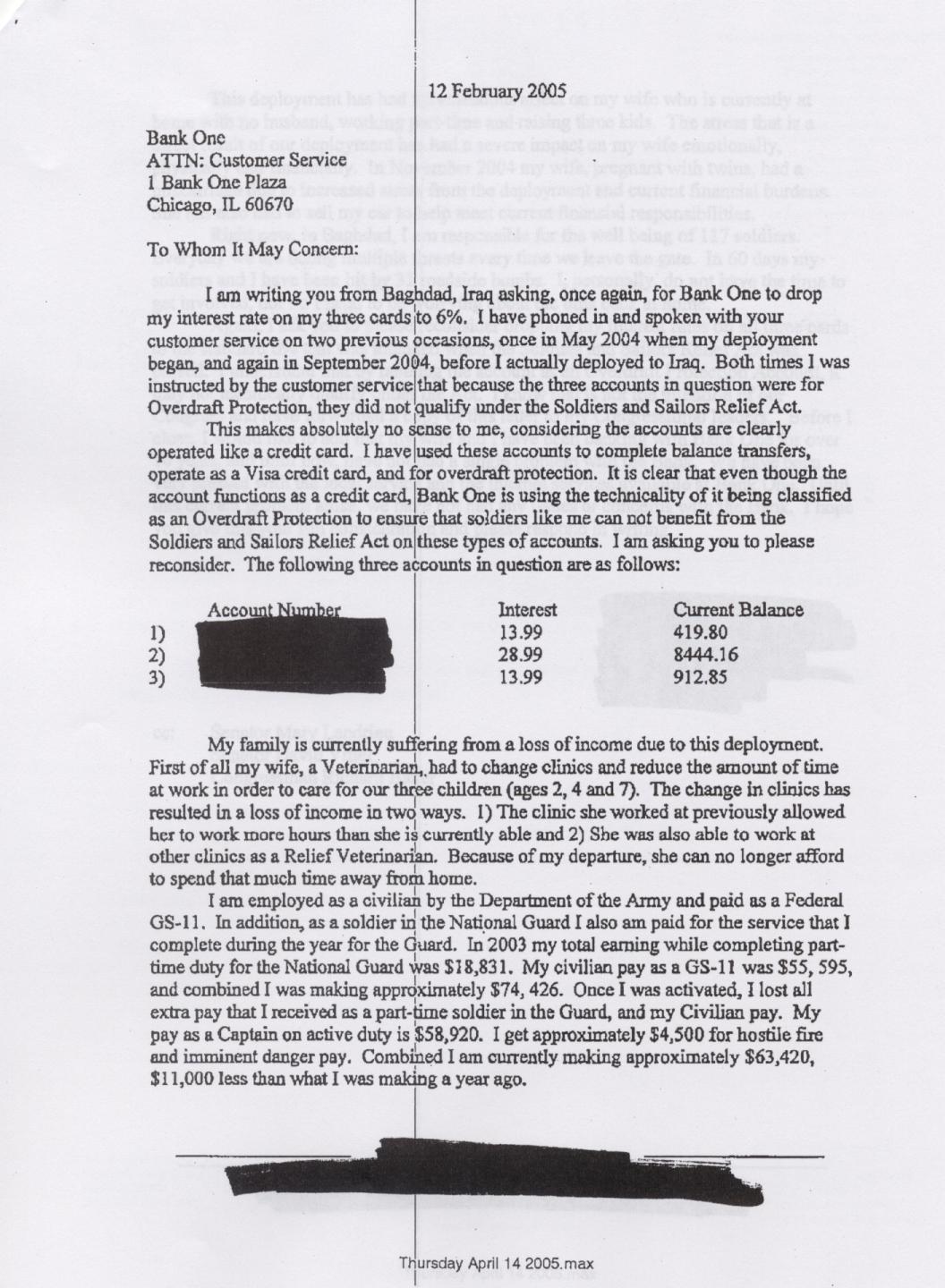

JP Morgan Chase’s

practices, and their impact on front-line military personnel, are

reflected in the complaint now online at

www.innercitypress.org/jpmcscra47a.jpg and

www.innercitypress.org/jpmcscra47b.jpg

“I am writing you from

Baghdad, Iraq asking, once again, for Bank One to drop my interest rate

on these three cards to 6%. I have phoned in and spoken with your

customer service on two previous occasions, once in May 2004 when my

deployment began, and again in September 2004, before I actually

deployed to Iraq. Both times I was instructed by the customer service

that because the three accounts in question were for Overdraft

Protection, they did not qualify under the Soldiers and Sailors Relief

Act. This makes no sense to me, considering the accounts are clearly

operated like a credit card. I have used these accounts to complete

balance transfers, operate as a Visa credit card, and for overdraft

protection. It is clear that even though the account functions as a

credit card, Bank One is using the technicality of it being classified

as an Overdraft Protection to ensure that soldiers like me cannot

benefit from the Soldiers and Sailors Relief Act on these type of

accounts. I am asking you to please reconsider. The following three

accounts in question are as follows:

Account 1 [REDACTED]

13.99% interest

Account 2 [REDACTED]

28.99% interest

Account 3 [REDACTED]

13.99% interest

…In November 2004 my

wife, pregnant with twins, had a miscarriage due to increased stress

from the deployment and current financial burdens. She has also had to

sell my car to help meet current financial responsibilities. Right now,

in Baghdad, I am responsible for the well being of 117 soldiers.

Everyday we are facing multiple threats every time we leave the gate. In

60 days my soldiers and I have been hit by 31 roadside bombs. I,

personally, do not have the time to get involved, nor do I need to be

worrying about the bills back home.”

The purpose of the Servicemembers’

Civil Relief Act is to provide interest rate relief and other

protections “to servicemembers of the

United States to enable such persons to devote their entire energy to

the defense needs of the Nation.”

50 USCS Appendix Section 502. Given the lack of compliance with

the SCRA by the above-named largest banks and bank holding companies,

Inner City Press / Fair Finance Watch has formally petitioned for action

from both the Office of the Comptroller of the Currency and the

Federal Reserve,

including by submitted copies of complaints of SCRA violations by Bank

of America and MBNA, and demanding that they be pursued prior to any

ruling other than denial on

Bank of America’s

application to acquire MBNA. ICP will be pursuing these issues

further.

For further information, click here to contact us

* * *

A related Inner City Press text:

Rights Force

A previous report, September 2005: The Federal Reserve

has announced the availability of final and aggregate 2004 Home Mortgage

Disclosure Act data.

www.ffiec.gov/hmcrpr/hm091305.htm The Fed also put forth its spin on

the data, in the form of 51-page study by staff members Bob Avery, Glenn

Canner and Robert Cook.

www.federalreserve.gov/pubs/bulletin/2005/3-05hmda.pdf While

the prose of the Fed's study is typically dense, here's the conclusion

the Fed reaches on the final page of its study:

…”black and Hispanic

borrowers taken together are much more likely than non-Hispanic white

borrowers to obtain credit from institutions that report a higher

incidence of higher-priced loans. On the one hand, this pattern may be

benign and reflect a sorting of individuals into different market

segments by their credit characteristics. On the other hand, it may be

symptomatic of a more serious issue. Lenders that report a lower

incidence of higher-priced products may be either less willing or less

able to serve minority neighborhoods. More troubling, these patterns may

stem, at least in part, from borrowers being steered to lenders or to

loans that offer higher prices than the credit characteristics of these

borrowers warrant. Reaching accurate determinations among these

alternative possible outcomes is one goal of the supervision system.”

What the Fed doesn’t say in this is that

these disparities are most stark some of the largest conglomerates in

the country, including in their headquarters cities (where they have

Community Reinvestment Act duties). As two example, with the largest

bank and thrift in the United States:

Citigroup in the

New York City Metropolitan Statistical Area in 2004 confined African

Americans seven times more frequently than whites to higher cost, rate

spread loans. The largest savings bank in the country,

Washington Mutual,

confined African American couples to high cost loans 4.5 times more

frequently than white couples, on nationwide basis. How could such

patterns be plausibly described as “benign” or as reflecting “a sorting

of individuals into different market segments”?

Where the rubber will meet the road will be in

how the Federal Reserve and other agencies act on specific disparities

at specific lenders, including as these are formally raised to them in

timely comments on merger applications. See, Inner City Press / Fair

Finance Watch's other studies of the 2004 HMDA

data: first second third fourth fifth. For or

with more information, contact us.

May 9, 2005

Inner City Press / Fair Finance Watch Completes

Analysis, by Gender as well as Race and Ethnicity, of Ten Large Lenders’ Mortgage

Disparities

May 9 -- ICP has

now comprehensively reviewed the 2004 Home Mortgage Disclosure Act data of the ten largest

lenders, by gender as well as race and ethnicity. ICP has compared each of these,

including not only denial rates but also the new information concerning which loans are

subject to a rate spread (3% higher than comparable Treasuries on a first lien, and 5% on

a subordinated lien, below referred to as subprime or high cost loans), and has found the

following:

At Washington Mutual, African American men were confined to high cost

loans 3.34 times more frequently than white men -- the largest disparity for this

comparison.

At Royal Bank of Canada / Centura, African American women were

confined to high cost loans 4.52 times more frequently than white men -- the largest

disparity. Wells Fargo was second most disparate to African American women, confining them

to high cost loans 4.31 times more frequently than white men.

At Bank of America, Hispanic men were confined to high cost loans

2.10 times more frequently than white men. White women were confined to high cost loans

2.04 times more frequently than white men -- the largest disparity for this comparison.

Again at Washington Mutual, Hispanic women were confined to high cost

loans 2.53 times more frequently than white men -- the largest disparity for this

comparison.

At Citigroup, for home purchase loans, African American

women were confined to high cost loans 4.06 times more frequently than white men. Hispanic

men were confined to high cost loans 2.15 times more frequently than white men; at Wells

Fargo, the disparity between Hispanic and white men was 1.78.

ICP has also provided evidence of

Citigroup’s violation of its commitment to have stopped, from January 2003

onward, making loans covered by the Home Ownership and Equity Protection Act of 1994

(eight full percent over Treasuries on a first lien mortgage, ten percent over Treasuries

on a subordinate lien). In the 2004 data, ICP

found that Citigroup reported fully 837 HOEPA loans. ICP

raised this to Citigroup’s senior management at the April 19 shareholders’

meeting at Carnegie Hall in Manhattan. Neither Citigroup chairman Sandy Weill nor CEO

Charles Prince would directly answer the question. Citigroup chief operating officer

Robert Willumstad directly denied that Citigroup had reported HOEPA loans in its 2004

data. Finally,

the New York Times of May 4, 2005, reported that “Citigroup lenders made

hundreds of high-cost home loans to customers with poor credit histories in 2004, even

though the company had adopted a policy a year earlier to no longer issue such loans, the

bank acknowledged yesterday.” ICP has now submitted

the specifics of Citigroup’s 837 HOEPA loans to the attorneys general in the states

in which these super high cost loans were made. See, www.innercitypress.org/citi.html

“The

largest bank is also the most duplicitous,” said ICP’s executive director

Matthew Lee. “Predatory and discriminatory lending are central to Citigroup’s

compliance problems, and we have asked for enforcement actions in more than twenty five

states.”

Regarding

Wells Fargo, ICP has received more and more complaints about Wells Fargo, including about

Wells’ stealth America’s Servicing Company unit. Wells Fargo is also a major

funder of payday lenders, including targeters of military personnel like Armed Forces

Loans. ICP has raised this directly to Wells Fargo, and to the Federal Reserve on Wells’

proposal to acquire First Community Capital Corp., which was announced back on September

2, was challenged by ICP on November 1, and which still remains pending, more than five

months later.

Regarding HSBC,

ICP’s filings with the states have also asked them to expand their $486 million

predatory lending enforcement action against HSBC / Household International to cover HSBC’s

Decision One unit, which made more subprime loans in 2004 than either HFC or Beneficial,

which are covered by the states’ settlement. ICP

has asked the attorneys general in more than thirty states to reopen their $486 million

predatory lending settlement with Household, and for example to make sure that it expands

to cover and require reforms from Household’s, now HSBC’s, Decision One subprime

lending unit.

ICP has also

now analyzed, because of the disparities identified above, the nationwide lending of he

Royal Bank of Canada:

Whites: 74,387

applications, leading to 5740 denials (7.72% denied) and 58,173

originations; 1971 [or 1.84 percent] exceeded rate spread.

African Americans: 4767 applications, leading to 612 denials (12.84% denied, 1.66

times higher than whites) and 3451 originations; 255 [or

7.39 percent] were at rate spread [3.99 times higher / more likely to be over rate spread

than whites].

Latinos: 8376 applications, leading to 870 denials (10.39% denied, 1.35 times

higher than whites) and 6105 originations; 163 [or 2.67

percent] at rate spread [1.45 times higher / more likely to be over rate spread than

whites].

ICP’s Matthew Lee said, “Royal Bank of

Canada bungled into buying Centura Bank, then a mortgage company based in Illinois, but

now runs both of them in a clearly disparate fashion.”

ICP has also

produced and submitted upon request to to New York State elected prosecutorial officials a

list of the largest subprime lenders in New York State, including among others New

Century, H&R Block / Option One, American Home Mortgage as well as the belownamed,

KeyCorp and other banks. Number one on the list is Ameriquest. ICP has also specifically

analyzed Ameriquest’s lending to Native Americans. Ameriquest confined over sixty

percent of Native American home purchase borrowers to higher cost subprime loans.

The

fact that Ameriquest, the increasingly discredited subprime lender admittedly under

investigation by twenty five states, in 2004 made the most loans to African Africans, both

over the high cost rate spread and overall, is a reflection of a two-tier financial

system, one which is separate and unequal, including as to interest rate. We have asked

for more than twenty five states to take action on Ameriquest.”

ICP has provide

this and other analysis to the regulators and state attorneys general, demanding

investigation and action. ICP has also requested action, from federal regulators and now

fifty state attorneys general, on lenders who have refused to provide data, and who

otherwise enable predatory lenders: Royal Bank of Scotland

and other subprime facilitators and securitizers (as reported in the London Sunday Times

of May 1), Lehman Brothers, Fifth Third, Delta Funding and AIG / American General (these

four and others have refused to provide their data in analyzable form), as well as Fremont

Investment and Loan, which is trying to require ICP to sign a confidentiality agreement to

view its public data. ICP has refused, and has filed complaints.

Methodology, Scope of Review

and Results

ICP Fair Finance

Watch reviewed the 2004 mortgage records (defined by the gender and race / ethnicity of

the primary applicant) of the above-named lenders, including the top five banks:

Citigroup

White men: 169,992 originations of which 37,974 (or 22.34%) were at

rate spread

White women: 67,291

originations of which 21,689 (or 32.23%) exceeded the rate spread (1.44 times higher /

more likely to be rate spread than white men)

African American men: 16,512 originations of which 8499 (or 51.47%)

exceeded the rate spread (2.30 times higher / more likely to be rate spread than white

men)

African American women: 16,116 originations of which 9099 (or 56.46%)

exceeded the rate spread (2.53 times higher / more likely to be rate spread than white

men)

Hispanic men: 22,757 originations of which 7393 (or 32.25%) exceeded

the rate spread (1.44 times higher / more likely to be rate spread than white men)

Hispanic women: 9241 originations of which 3649 (or 39.49%) exceeded

the rate spread (1.77 times higher / more likely to be rate spread than white men)

JP Morgan Chase

White men: 241,337 originations of which 12,594 (or 5.22%) were at

rate spread

White women: 92,764 originations of which 6899 (or 7.44%) exceeded

the rate spread (1.43 times higher / more likely to be rate spread than white men)

African American men: 16,654 originations of which 2306 (or 13.85%)

exceeded the rate spread (2.65 times higher / more likely to be rate spread than white

men)

African American women: 14,684 originations of which 2263 (or 15.41%)

exceeded the rate spread (2.95 times higher / more likely to be rate spread than white

men)

Hispanic men: 32,669 originations of which 2188 (or 6.70%) exceeded

the rate spread (1.28 times higher / more likely to be rate spread than white men)

Hispanic women: 13,490 originations of which 1021 (or 7.57%) exceeded

the rate spread (1.45 times higher / more likely to be rate spread than white men)

Bank of America

White men: 270,5012 originations of which 4854 (or 1.79%) were at

rate spread

White women: 110,816 originations of which 2259 (or 2.04%) exceeded

the rate spread (1.14 times higher / more likely to be rate spread than white men)

African American men: 15,843 originations of which 588 (or 3.71%)

exceeded the rate spread (2.07 times higher / more likely to be rate spread than white

men)

African American women: 14,352 originations of which 561 (or 3.91%)

exceeded the rate spread (2.18 times higher / more likely to be rate spread than white

men)

Hispanic men: 49,884 originations of which 1875 (or 3.76%) exceeded

the rate spread (2.10 times higher / more likely to be rate spread than white men)

Hispanic women: 18,598 originations of which 783 (or 4.21%) exceeded

the rate spread (2.35 times higher / more likely to be rate spread than white men)

Wells Fargo

White men: 554,755 originations of which 36,012 (or 6.49%) were at

rate spread

White women: 196,396 originations of which 21,514 (or 10.95%)

exceeded the rate spread (1.69 times higher / more likely to be rate spread than white

men)

African American men: 29,858 originations of which 6357 (or 21.29%)

exceeded the rate spread (3.28 times higher / more likely to be rate spread than white

men)

African American women: 25,278 originations of which 7067 (or 27.96%)

exceeded the rate spread (4.31 times higher / more likely to be rate spread than white

men)

Hispanic men: 55.126 originations of which 5763 (or 10.45%) exceeded

the rate spread (1.61 times higher / more likely to be rate spread than white men)

Hispanic women: 19,276 originations of which 2843 (or 14.75%)

exceeded the rate spread (2.27 times higher / more likely to be rate spread than white

men)

Wachovia

White men: 92,209 originations of which 3428 (or 3.72%) were at rate

spread

White women: 36,684 originations of which 1806 (or 4.92%) exceeded

the rate spread (1.32 times higher / more likely to be rate spread than white men)

African American men: 9011 originations of which 926 (or 10.28%)

exceeded the rate spread (2.76 times higher / more likely to be rate spread than white

men)

African American women: 7912 originations of which 827 (or 10.45%)

exceeded the rate spread (2.81 times higher / more likely to be rate spread than white

men)

Hispanic men: 7400 originations of which 390 (or 5.27%) exceeded the

rate spread (1.42 times higher / more likely to be rate spread than white men)

Hispanic women: 3462 originations of which 253 (or 7.31%) exceeded

the rate spread (1.97 times higher / more likely to be rate spread than white men)

Beyond its

filings with fifty state attorneys general, ICP is also commenting to, and also litigating

Freedom of Information Act issues against, federal agencies like the Federal Reserve

Board, in connection with Wachovia’s support of payday lenders and other fringe

financial institutions, see, e.g., Dow Jones of

October 25, 2004, “Community Group: Fed Must Reconsider Wachovia-SouthTrust”).

ICP's book on these topics, "Predatory Bender"

CL

Review order / Amazon

For further information, click here to contact us

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}